The past few years have seen more than the usual amount of political upheaval. But, interestingly, most regime changes have resulted in pretty much the same thing: Higher government spending and bigger deficits.

Apparently the only “reforms” today’s voters will accept – which is to say the only actions that don’t get a leader kicked out of office – involve spending rather than saving money.

Three recent examples:

The US

Republicans – the party of smaller government – gained control of the White House and Congress in 2016, and proceeded to take a meat ax to bloated entitlements, lowering the government’s share of the economy to levels not seen since the Reagan years.

Just kidding. They tried to eliminate the newest entitlement, Obamacare, but failed to produce even a coherent proposal. So instead they cut taxes, expanded the military and left everything else on autopilot. Now, nine years into a recovery with official unemployment below 4% — and with the small-government party in charge:

U.S. budget deficit approaches $1 trillion

(MarketWatch) – The Treasury Department says that adjusted for timing-related transactions, the deficit would have been $270 billion over the last two months compared to $250 billion during the same period the prior year, with tax revenue up by 1% but spending up by 4%.

The budget picture is deteriorating as the U.S. taxes individuals and companies less and spends more, mostly on defense and benefit payments to an aging population. Though a growing economy is softening the blow, it’s possible that the annual deficit will top $1 trillion this year.

Italy

Voters recently installed a coalition of left and right-wing populists who immediately tried to make good on a number of campaign promises while ignoring the EU’s deficit guidelines. Threats flew and bond yields spiked, making it clear that the new government would have to be more circumspect. So Rome promised to keep its spending within EU limits. However…

Italy’s Budget Pledge Is Just Cosmetic

(Bloomberg) – Italy’s populist government has pledged to the European Commission that it will lower its deficit target to 2 percent of national income next year. For a cabinet that vowed to defy the “bureaucrats” in Brussels, this is a stunning climb-down. But unless Rome is ready to row back on some of the key pledges included in its 2019 budget, it will amount to little more than cosmetic change.

So when prime minister Giuseppe Conte told reporters on Monday that Italy would now target a 2.04 percent deficit, this was indeed a remarkable U-turn.

The markets shouldn’t celebrate too soon, though. For a start, Di Maio and Salvini have yet to utter a word about what Conte has said. In most other countries, a prime minister doesn’t have to wait for his two deputies to confirm that his words have value. But in the strange coalition arrangement that rules Rome, this is certainly the case.

Moreover, details matter. In a sense, the 2.4 percent deficit target for next year wasn’t the main problem with Italy’s budget. Worse is the wildly optimistic growth target, which means that borrowing will probably be much higher than predicted. Then you have the non-credible budget deficit targets for the following two years, which rely on VAT increases that no one believes in. Finally, there’s the decision to keep the structural deficit unchanged between 2019 and 2021, instead of aiming to reach a balanced budget over the medium run. For a country whose public debt stands at more than 130 percent of GDP, these are hardly details.

France

New president Emmanuel Macron tried to modernize the laughably hidebound French labor markets. But it blew up in his face, as tens of thousands of protestors took to the Paris streets in a conflagration that generated global headlines and raised questions about Marcon’s political future.

Macron’s response? Higher spending, of course:

Macron’s credibility shattered as France joins Italy in budget disgrace

(Telegraph) – Emmanuel Macron’s bid to buy off France’s “gilets jaunes” protesters with instant budget handouts threatens to blast through eurozone’s fiscal limits, fatally damaging his credibility as the champion of the European project and the guardian of French public accounts.

The package of short-term measures announced in a theatrical mea culpa on Monday night leaves President Macron’s putative “grand bargain” with Germany in tatters.

He had pledged root-and-branch reform of the French economy and a restoration of spending discipline after 11 years in breach of the EU’s Stability Pact. The calculation was that Berlin would in return drop its long-standing opposition to fiscal union and shared liabilities, agreeing to rebuild the euro on stronger foundations.

To the extent that this bargain was ever more than wishful thinking, it is dead now. The German Kanzleramt and finance ministry have watched near insurrection sweep the major cities of France over the last four weeks – with “Act V” already announced for next weekend – and watched a belated riposte from Élysée Palace that amounts to a climbdown.

“Macron’s response suggests that a rioting and pillaging mob can dictate politics, while those who demonstrate peacefully – or not at all – are ignored,” said Clemens Fuest, president of Germany’s IFO Institute. “His whole ability to push has been called into question. What he has announced are just tax giveaways.

“It is quite obvious that the budget deficit will be at least 3.5pc of GDP next year, and probably 4pc because the economy is heading for a light recession,” said Professor Jacques Sapir from the École des Hautes Études en Sciences Sociales in Paris.

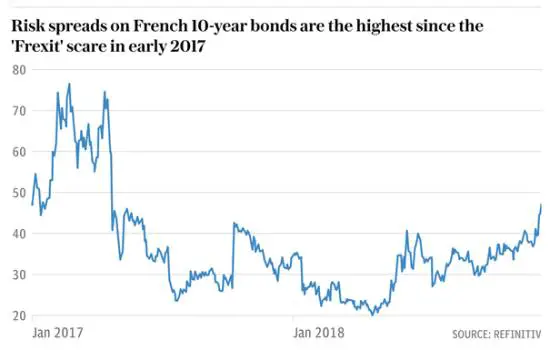

Risk spreads on French 10-year debt jumped to 48 basis points on Tuesday as bond vigilantes began to digest the scale of fiscal slippage. This is the highest level since the ‘Frexit’ scare before the French elections in early 2017, when the Front National’s Marine Le Pen was riding high in the polls.

Kallum Pickering, from Berenberg Bank, said Mr Macron has “turned from darling to fallen angel very quickly”. The cancellation of the fuel tax rise and latest sweeteners will together cost €14bn. “France’s debt-to-GDP will likely rise beyond 100pc as a result,” he said.

Macron’s travails have broader implications. From the above Bloomberg article on Italy:

The [EU] Commission is in an awkward spot. The decision by Emmanuel Macron, France’s president, to pass a string of tax cuts and spending increases to appease the “Yellow Vest” protesters has made it politically harder to move against Italy without smacking of hypocrisy. But if Brussels were to accept a few cosmetic changes from Rome without any real substance, its already shaky reputation as the enforcer of the bloc’s fiscal rules would be in tatters.

So the poker game between Brussels and Rome goes on. It’s just that both players have far fewer chips than they originally assumed.

Keep in mind that all this is happening in an expansion. During the next recession, expect government spending and deficits around the world to soar to stunning levels, raising questions about the viability of not just presidents and prime ministers, but of currencies.

22 thoughts on "All (Political) Roads Lead To Massively Higher Government Spending"

I basically make close to $6,000-$8,000 a month online. I lost my job after doing work for the same company for a long time, I required trusted earnings, I was not researching for the “get rich quick” home programs you see all over the net. Those are usually pyramid schemes or stuff in which you have to sell to your friends and relatives. I basically wanted a legitimate way to earn a living for me and my family. The most important part of working on line is that I am always home with the children and also enjoy time with family on different beaches of the world. All you need to do is submit a very simple form to obtain front line access to the Home Profit System . You don’t need to be a computer whiz, but you should know how to use the net. If you can fill up forms and browse websites, you can do it quite easily, You don’t even have to sell anything at all and no one has to purchase anything.Here’s how you can get started=> https://iplogger.org/2L8Cj5

I generally gain around $6,000-$8,000 a month via internet. It is really adequate to comfortably replace my old jobs income, specially considering I just work about 20 hrs each week at home.I lost my job after doing work for the same company for years, I needed trustworthy earnings, I was not thinking about the “get rich quick” home programs you notice all over the net. Those are typical pyramid schemes or stuff where you need to sell to your friends and relatives. I basically wanted a legitimate way to earn a living for me and my family. The most interesting part of working on line is that I am always home with the kids, I save a good amount of money. Honestly,it is simpler than you would believe, all you have to do is fill out a simple form to receive front line access to the Home Profit System . You don’t need to be a computer whiz, but you should know how to use the net. If you can fill up forms and surf web sites, you can do it quite easily, You don’t need to sell anything and no-one needs to buy anything . It’s as easy as being on Facebook.Here’s how you can start out>>> READ REVIEWS

I generally generate nearly $6,000-$8,000 on a monthly basis through online. It is really more than enough to easily replace my old jobs salary, especially considering I only work about twenty hr weekly at home.I lost my job after working for the same organization for several years, I needed trusted earnings, I was not researching for the “get rich quick” home programs as you can see online. Those are usually pyramid schemes or stuff where you have to sell to your friends and family members. I basically needed an authentic method to earn a living for me and my family. The most important part of working via internet is that I am always home with the kids, I save lots of money. Honestly,it is simpler than you would think, all you have to do is fill out a simple form to receive front line access to the Home Profit System . You don’t need to be a computer whiz, but you should be aware how to use the net. If you can fill up forms and browse web-sites, you can do it quite easily, You don’t need to sell anything at all and no one needs to buy anything . It’s as simple as being on Youtube.Here’s the right way to start>> START NOW GET RESULTS

I actually earn nearly $6,000-$8,000 monthly online. It’s enough to easily replace my previous jobs earnings, especially considering I just work about twenty hr a week from home.I lost my job after doing work for the same company for years, I required trustworthy income, I was not thinking about the “get rich quick” home programs as you can see all over the internet. Those are typical pyramid schemes or stuff in which you need to sell to your friends and family. I actually wanted a trustworthy way to earn a living for me and my family. The most exciting part of working on-line is that I am always home with the kids, I save a good amount of money. Honestly,it is simpler than you would believe, all you need to do is submit a simple form to receive front line access to the Home Profit System . You don’t need to be a computer whiz, but you should be aware how to use the net. If you can fill up forms and browse sites, you can do it very easily, You don’t need to sell anything and no one has to buy anything . It is as simple as being on Facebook.Here’s how you can start out—> CONTACT US

Achievement meets those who constantly work hard and in a smart way and make use of opportunity in a proper manner. A career which is online and provides you enough time to devote with those you love and you can get almost $41000 regular monthly. Really easy work where you don’t require any kind of technical knowledge. It is reliable and authentic and definitely not like any cheats you find all over the internet. You are required to devote couple of hours and can make a very good income. Dream big and be an achiever. Go and visit this phenomenal online based job without any delay.>>>>>>>> https://ynusava.tumblr.com

Opportunity never knocks the door twice, It truly is essential to make full usage of the opportunity. A work which gives you complete liberty to work from home. Job opportunity that is online and you need to simply commit a handful of time into the work. It surely is not similar to false promises you will see on on-line that claims to make you millionaire and later turned out to be some fraud selling schemes. It really is real and reliable. It is simple to begin and it also enables you to get excellent income. Be your own boss and devote a lot more valuable time with the people you care about and get approximately $46000 each and every month. It is time for you to take a look at this opportunity and transform your life forever >>>>>>>>>>>>> https://bit.ly/2MjmCcG

Make 90 dollars /daily for working over the internet from your home office for several hrs /day… Get paid regularly on a weekly basis… You’ll need a laptop, internet connection, along with some leisure time… Superb thing about this job is the more free time I got with my kids. I am able to spend quality time with my family and friends and take care of my babies and also going on holiday along with them very often. Don’t ignore this chance and try to respond rapidly. Here is what I do START WORKING IMMEDIATELY!!!

Exploring all across the world is a wonderful and fascinating dream. We work all day long in our company to turn this dream into reality. However how many truly able to make money? We bring to you, this amazing web-based opportunity created in a way that it helps you to earn great money. Work on a daily basis and give your work small amount of hours and get approximately $43000 every week. It provides you opportunity to work from anywhere with extremely flexible time and able to devote some quality time with all your family. The time has come to convert your life and bring growth and prosperity. Right now go and take a look at, awesome things waiting for you >>> SUPERB OPPORTUNITY!!!

You will discover numerous online jobs that currently are available. And, in today’s world, there are many opportunities using the net, and this craze is predicted to continue well into the future. Who would not desire to work from home on a part-time basis and bring in 1000s of dollars on a monthly basis? This is an offer the majority of people can’t or don’t resist. So,today I am going to tell you a wonderful home-based opportunity from which you can make between 5000 dollars to 10000 dollars every 30 days. Here’s what I do ->->-> SUPERB OPPORTUNITY!!!

There are tons of work-at-home job opportunities that currently available. And, in today’s world, there are many job opportunities using the internet, and this emerging trend is expected to keep going very well in the future. Who wouldn’t choose to work from home on a part-time basis and bring in thousands of dollars each month? It is an offer lots of people can’t or don’t refuse. So,now I am going to tell you an awesome internet opportunity from which you could earn between 5k dollars to 10k dollars every 30 days. This is what i do… >> NICEST WORK!!!

There are plenty of working at home job opportunities that really are available. And, in today’s surroundings, there are way more job opportunities via the internet, and this trend is expected to keep going on well ahead. Who wouldn’t desire to work at home on a part-time basis and receive 1000s of dollars every 30 days? This is an offer many people can’t or do not resist. So,now Let me tell you a brilliant home-based opportunity from which you could earn between 5000$ to 10000$ a month. Check it out, what it is about… >>>> NICEST WORK!!!

You will discover numerous home based job opportunities that presently exist. And, in today’s marketplace, there are many jobs on the internet, and this trend seems to prolong nicely into the future. Who would not desire to work from home on a part-time basis and earn 1000s of dollars every 30 days? It is an offer the majority of people cannot or do not avoid. So,today I am going to tell you an impressive home based job opportunity from which you are able to profit between 5000$ to 10000$ on a monthly basis. Let me show you what i do… ->-> NICEST WORK!!!

I commonly benefit almost 6,000 to 8,000 dollars each and every 30 days using the internet. It is usually more than enough to doubtlessly replace my past professions net earnings, primarily seeing that I only do the work nearly 20 hours each week from home.I dropped my job after working for the same employer for several years, I needed trustworthy profit, I was not exploring for the “get rich quick” home kits as you can see across the net. Those are typically pyramid plans or things where you really need to sell to your neighbors and persons in the family. I truly required a reliable program to make money for me as well as my family. The greatest benefit of doing the job via internet is that I am normally home with the children, I save good money. Indeed, it is simpler than you could think, all that is needed is fill up an easy application form to obtain front line entry to the Home Earnings Program. I obtained the instructions kit and within 30 days I began generating over $4,000 per month. The guidelines are incredibly simple, you don’t have to be a computer expert, but you must understand how to use the net. If you are able to fill forms and browse internet sites, you are able to do it easily, You need not even have to sell off anything and nobody have to buy anything. It is really as simple as using Youtube or twitter.Here’s the ultimate way to start >> NICEST WORK!!!

I frequently get somewhere around $17,000-$18,000 each and every month from the internet. After working so wholeheartedly, I ended up losing my job in my company where I have given so many years. I truly required a reliable income source. I am not into “get rich overnight” package deals as you can see all over the internet. Those are all kind of ponzi referral marketing schemes in which you need to first make interested customers and then sell a product to friends and family members or any person so that they will probably be in your team. Web work provides many benefits such as I am always home with my loved ones and can really enjoy lots of free time and go out for family trips. Here’s the easiest way to start >>> https://kadvent.tumblr.com

One yr have passed since I abandoned my office work and I couldn’t be happier now…. I started to work online, for a company I stumbled upon over internet, few hrs a day, and I profit now much more than I did on my previous job… My paycheck for last month was $9k… The best thing about it is that now I have more free time with my kids…and the only thing required is simple typing skills and connection to the internet… I am in a position to spend quality time with my relatives and buddies and look after my babies and also going on vacation along with them very frequently. Don’t neglect this chance and try to act fast. Here is what I do see important info

One year ago I decided to leave my previous job and it changed my life…. I started to work over internet, for this company I found online, for a few hours daily, and I make much more than I did on my previous job… My check for last 30 days was $9k… Superb thing about this work is that I have more free time with my kids…and that the only requirement for being able to start is simple typing skills and internet access… I am in a position to dedicate quality time with my friends and family and take care of my babies and also going on holiday vacation with them very frequently. Don’t miss this opportunity and try to act quick. Let me show you what I do… see detailed info right now

It’s been one year since I decided to leave my office job and that decision was a life-changer for me…. I started doing work on-line, for this company I found online, few hrs each day, and I profit now much more than I did on my last work… My paycheck for last 30 days was 9,000 US dollars… The best thing about it is the more time I got for my loved ones…and that the only requirement for this job is simple typing and reliable internet… I am able to devote quality time with my family and friends and take care of my children and also going on holiday vacation along with them very routinely. Don’t skip this chance and make sure to react quickly. This is what I do… act now by clicking here

It’s been one yr since I abandoned my previous job and I never felt this good…. I started to work from comfort of my home, for a company I stumbled upon over internet, for a few hours every day, and my income now is much bigger then it was on my last work… My paycheck for last 30 days was 9,000 dollars… Awesome thing about this work is the more time I got with my family…and the only thing required is simple typing skills and internet connection… I am able to commit quality time with my family and friends and look after my babies and also going on holiday along with them very routinely. Don’t miss this opportunity and try to respond quickly. This is what I do… see this

“If something can’t go on forever it will stop.”

— Herbert Stein

One way or the other over the next 10 to 20 years every welfare state is going to go “stop”.

This video explains what happened after the old order “stopped” at the end of WW1. It became a mad scramble for control by upstarts and new ideas all around the world. Absolutely fascinating. https://www.youtube.com/watch?v=pNoF5gNLrzA

If you are wanting to produce $8175 month to month by just utilising your very own online connection coupled with notebook then I must tell you about my benefit from. 24 months back in the past I have been being employed in commercial enterprise without being paid safe earnings matching my difficult work. Soon after my best friend told me to focus on an on line business which can be done at comfort of home with the help of website and computer and great thing about it that it is possible to perform any time we desire and enjoy the funds on week after week basis. It’s different from a fraud that you may watch all over the internet that offers to make you ultra wealthy in 2 to 3 days or so. Currently after using this earning opportunity for two years I can that this is certainly the perfect internet based business I can secure because of the fact that by working on this venture I am able to work when ever I am able to. While I was working through private job I was unable to get some more free time with my loved ones but these days during twenty four months I am dealing with this web-based occupation and from now on I am taking pleasure of the leisure time with my friends and family at home or simply by going outside to any spot I enjoy. This chore is often as trouble-free just like going to webpages and conducting copy-paste paste job that everyone is able to do ->->-> sulfidegarlicky.allemal.de

It’s been 1 year since I finally left my previous work and I couldn’t be happier now…. I started doing a job from my house, for this company I discovered over internet, few hours daily, and I profit now much more than I did on my last work… My check for last 30 days was 9,000 dollars… The best thing about this gig is that now I have more free time to spend with my family…and that the only requirement for to get started is simple typing and connection to the internet… I am in a position to commit quality time with my friends and family and look after my babies and also going on family vacation along with them very frequently. Don’t let pass this chance and make sure to respond rapidly. Here’s what I do find out here

$9,000 in 30 days? That’s not worth it – not for typing. I hate typing.