The euro system and its currency are descending into crisis. Comprised of the ECB and the National Central Banks, the system is over its head in balance sheet debt, and it is far from clear how that can be resolved. Therefore, the euro is sliding. Markets can see that all the ECB is doing is talking the talk and otherwise is frozen into inaction…

by Alasdair Macleod on Goldmoney:

Normally, a central bank is easy to recapitalise. But in the case of the euro system, when the lead institution and all its shareholders need to be recapitalised all at the same time the challenge could be impossible. And then there’s all the imbalances in the TARGET2 system to resolve as well before national legislatures can sign it all off. Additionally, but part of the TARGET2 problem there’s the repo market with €8.7 trillion outstanding, set to implode on rising interest rates, destroying commercial bank balance sheets which are already highly leveraged.

This goes some way to explaining the deep reluctance the ECB has about raising interest rates. While producer prices in key member states are rising at over 30% year-on-year, and consumer prices by over 8%, the ECB keeps its deposit rate at minus 0.5%. It knows that if euro bond yields go any higher their situation which is already untenable will disintegrate into a full-blown crisis.

Therefore, the euro is sliding. Markets can see that all the ECB is doing is talking the talk and otherwise is frozen into inaction.

Fiddling while Rome burns…

At a political level there appear to be terrifying levels of ignorance about the economic consequences of continuing to punish Britain for Brexit (yes, that still rankles) and now ostracising Russia for its belligerence at a time when the EU’s own economy is teetering on the edge of a financial and economic catastrophe. The EU exercises its political agendas despite any economic mayhem created.

Russia is a far more serious issue than Brexit ever was. The EU has, to varying degrees, disposed of its fossil fuel capacity to placate environmentalists, exporting their production to nations not so squeamish about fashionable climate change strictures. Consequently, the EU has become highly dependent on Russian natural gas and oil, which in cavalier fashion it has decided to do without to punish Russia over its invasion of Ukraine.

The economic consequences have been to put Germany’s economy on life support with its industrial limbs beginning to shut down, along with the productive capacity of many other EU states. In the coming months there will be food shortages exacerbated by lack of fertiliser supplies. Then there will be winter without heating fuel and frequent power cuts. And winter with food shortages in a continental climate is no joke. They will spark riots and growing political instability.

The financial consequences stem partly from bank exposure to Russian entities, but far more important is the effect of soaring producer and consumer prices on the entire Eurozone financial structure. The euro system has depended on redistributing wealth from Germany and the fiscally conservative northern states to bail out the profligate south using suppressed interest rates. That scheme is now kaput.

The ECB, and the euro system of shareholder national central banks, has metaphorically been caught with their collective trousers down. Having suppressed interest rates into negative territory, they allowed member governments to borrow ultra-cheaply. Now that Eurozone CPI is rising at 8.6% and Germany’s producer prices are up 33.6%, either interest rates must rise smartly or the euro crashes. Our headline chart of the euro/dollar rate at the top of this article refers to the market’s reaction so far.

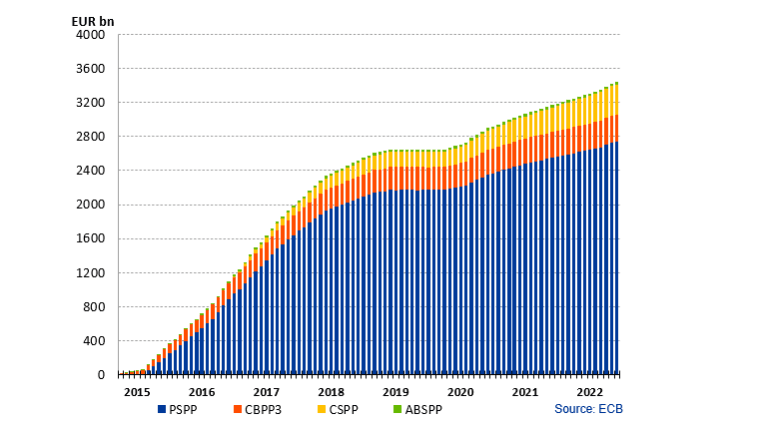

Bonds in the ECB’s Asset Purchase Programme have accumulated as shown in the chart below, split out into the Public Sector Purchase Programme (PSPP), Corporate Sector Purchase Programme (CSPP), Asset-backed Securities Purchase Programme (ABSPP) and the Third Covered Bond Purchase Programme (CBPP3). In June, they totalled €3,265,172 million.

From a year ago, government bonds have risen in yield from minus 0.5% to 1.36% for Germany’s 10-year bond, an overall rise of 1.86%. The rise in yield for a similar Italian bond is 2.87%, Spain’s 2.3%, France’s 2%, and Greece’s 3.2%. Given that government stock is 65% of the total, the rest being generally higher yielding corporate bonds, a conservative estimate is that if the portfolio has an average maturity of ten years the mark-to-market loss from a year ago is already in the region of €750bn. This is almost seven times the combined euro system balance sheet equity and reserves of €109.272bn. And as yields rise further, euro system losses of double that are easy to imagine.

Doubtless, if challenged the ECB would claim the euro system will hold these bonds to maturity, so they will continue to value them at par. But the euro system is unlikely to cease funding member states by inflationary means. And we cannot ignore the likelihood of further rises in yield due to the disparity between current interest rates (the ECB’s deposit rate is minus 0.5%) and a CPI heading towards annual increases of 10%…

The ECB and its impossible task

So far, we have laid bare the consequences of the energy crisis for the eurozone economy and the losses that arise on the euro system balance sheets. Overseeing it all is the ECB’s president, who previously served as Chair of the IMF and before that held roles in the French government, including economy and finance minister. With this experience she was appointed to the ECB as a safe pair of hands. And as such, she has inherited an impossible position, because she has no mandate to moderate the ECB’s inflationary policies.

More correctly, Lagarde inherited two impossibilities. The first is to continue to distribute Germany’s national wealth to support the PIGS, and the second is a banking system that is well and truly broken. And as stated earlier, Germany itself is now on life support….

Along with Luxembourg, Germany is the biggest loser in the arrangement. Germany’s equity ownership in the ECB is 21.44% of its capital.[i] If TARGET2 collapsed, the Bundesbank would lose over a trillion euros owed to it by the others and the ECB itself, and pay up to €387bn of the net losses, based on current imbalances. It would wipe out the Bundesbank’s own balance sheet many times over….

The euro system member with the greatest problem is Germany’s Bundesbank, now owed well over a trillion euros through TARGET2. The risk of losses is set to accelerate rapidly because of repeated rounds of Covid lockdowns in the PIGS and now with the Ukraine situation….

But the problem remains: as a mechanism that permits the PIGS to shelter nonperforming loans in increasing quantities, the TARGET2 setup has become rotten to the core and off the record is known to be. And now, thanks to the economic impact of the coronavirus followed by Ukraine, sooner rather than later the settlement system is set to fail completely.

Until then, TARGET2 is a devil’s pact which is in no one’s interest to break…. The sheer scale of a TARGET2 failure makes a resolution appear impossible…. No one knows how it would work out because failure of the settlement system was never contemplated; but many if not all of the national central banks would have to be bailed out, presumably by the ECB as guarantor of the system…. The ending of TARGET2 is therefore likely to be a complete write-off for the national central banks and will mark the end of the ECB….

The above article is an abridged version. You can read the full article on Goldmoney.

Tin Is A Critical Metal In the Green Energy Revolution

Every component of the carbon reduced and growing data-driven economy requires tin and this “critical metal” has outperformed most green energy metals over the past 12 months. This recently listed company has a high-quality portfolio of tin projects and has an aggressive exploration plan with positive results already announced! Don’t miss your opportunity.

Add this company to your watchlist