So many patterns that have held for decades seem to have broken down, leading to one of two conclusions: Either this time really is different in ways that appear to violate what used to be seen as iron-clad laws of finance, or those laws have been bent but will reassert themselves with a vengeance sometime in the future.

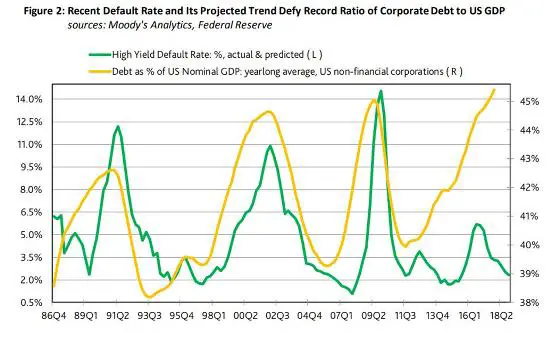

The latest example is the relationship between corporate debt and default rates on that debt. Historically they’ve moved in the same direction, with higher debt levels leading to higher default rates. That makes intuitive sense because rising debt implies that borrowing is easier for less creditworthy companies who should be expected to default at a higher rate.

But not this time:

Here’s why default rates are subdued even as corporate debt levels hit records

(MarketWatch) – U.S. corporate debt levels stand above crisis highs even as default rates among the most leveraged firms remain subdued.

With an economy hitting its stride, it’s perhaps no surprise that the high-yield bond market is placid. The extent of the divergence between debt levels and defaults, however, is worrying to some analysts who feel rising corporate indebtedness will eventually catch out unwary investors and deflate the junk-bond market.

But beyond complacency John Lonski, chief economist at Moody’s Capital Market Research, argued that globalization and the tendency of U.S. businesses to hoard cash as reasons why corporate debt levels may no longer move in sync with default rates and credit spreads.

The high-yield default rate in the fourth-quarter of 2017 fell to 3.3%, even as U.S. nonfinancial-corporate debt ended in 2017 at 45.4% of GDP. This compares with a much higher default rate of 11.1% in the second quarter of 2009, with corporate debt levels at 45% of GDP. Granted, the current levels come with the economy in the eighth year of an expansion, while the second quarter of 2009 marked the final quarter of the longest and deepest U.S. recession since the Great Depression.

The yield spread between high-yield bonds and safe government paper, as represented by the 10-year Treasury note narrowed to an average 3.63 percentage points in the fourth quarter of 2017, from an average 12.02 percentage points in the second quarter of 2009. The tight credit spreads reflects that borrowing costs are still close to historic lows, and that investors are demanding minimum compensation for holding arguably the riskiest debt in the bond market.

Moody’s Analytics

One answer “might be supplied by the ever increasing globalization of U.S. businesses where the more relevant denominator is not U.S. GDP, but world GDP” said Lonski.

The fortunes of U.S. companies are now woven into the broader global economy. When commodity prices took a hit in 2015 and early 2016, crimping growth in China and other emerging markets, high-yield bonds were also slammed.

With commodity prices on the rise and global growth making a comeback, it’s no mystery that issuers of high-yield bonds aren’t in any serious trouble.The tendency of U.S. corporations to accumulate cash could also be to blame. Lonski says net corporate debt to GDP, which subtracts total debt levels by the amount of cash in business balance sheets, was at a much more subdued 33.2%, well below the 45.2% seen in the broader debt to GDP measure.

But the meaningfulness of this statistic may be limited by the “high concentration of cash among relatively few companies,” many of which are considered highly creditworthy.

Tech companies like Apple and Microsoft have been the main components of this trend. In the past, such firms issued debt backed by the collateral of their overseas profits for share buybacks and other forms of shareholder remuneration.

So has the correlation between corporate debt and defaults been broken for good or just for now? “Just for now” remains the most likely answer, since the business cycle is embedded in human nature rather than some kind of external constraint that we can evade with clever tricks. In fact, it’s clever tricks – like the fiat currency printing press — that fool us into thinking we control events that used to control us.

And is it worth speculating about what might happen to restore those historical relationships – that is, cause a crisis that spikes junk bond defaults and causes corporate debt to start shrinking? Probably not, since there are so many candidates right now. Something will happen and the lines on the above chart will converge in the upper right corner – and then the bottom right.

23 thoughts on "Yet Another Chart That Screams “Look Out!”"

Even Bloomberg TV reporters are forbidden to discuss the real unemployment and the real inflation as it affects incomes under $75,000 a year. They openly admid it is a paradox of why wages are not keeping up with inflation.

All of the mis-information creates a cluster of narrow-minded thinking.

When everyone in the financial news room thinks the same, then nobody is really thinking.

As of 2015, just 30 firms accounted for half the profits of all publicly-listed U.S. companies, down from 109 in 1979. Only by accumulating debt have many laggards been able to afford the buybacks necessary to keep stock appreciation stable. The IMF warned last year that 22% of U.S. corporations are at risk of default if interest rates rise.

Below is the link to the second part of a two-part series. The first explored how stock buybacks have been instrumental in driving this market higher since QE fueled easy money starting in 2009. This part focuses on what is ahead and how the recently passed Trump tax plan has supercharged this trend just as it may have been reaching its natural conclusion.

http://brucewilds.blogspot.com/2018/03/stock-buybacks-driving-market-where-it.html

All this shows me is that there are a lot of zombies out there and as a result, a stupendous amount of malinvestment in the economy. In “normal” times, “normal” rates of interest set a bar which assures that only the most efficient stay in business, while the failures’ assets get recycled through the capitalist apparatus. Unfortunately, nowadays we are in an economy that can be described as “capitalist” in name only.

This BTW could also help explain why productivity growth has been so weak.

Another explanation is that since borrowing costs are so low and the desire for investment returns so high that any corporation that might be in danger of missing its bond interest payments can simply borrow more to pay them.

It’s sort of like the scenario in the TV G. Versace drama series in which a guy who owed a bundle to American Express explains that if they would simply approve the purchase of a plane ticket to Minneapolis he would be able to get the money he owes – and they did it!

Bruce, that’s exactly how it works. At the peak of a cycle everyone has money to lend and is desperate for yield so even weak companies can refinance their debt and defaults are rare. But when money starts to get tight (usually because the Fed is raising rates to keep inflation from accelerating) the weakest borrowers get cut off and can’t refinance. They fail and that starts a chain reaction that sends junk defaults from 3% to 10%. At which point no one wants to touch junk bonds and the cycle begins again. What’s odd is that it still comes as a surprise to so many people who should know better.