Editor’s note: I’m including this older article by Wolf Richter today because it helps explain why today’s CPI does not reflect soaring rent increases that have actually happened or the rapid rise in housing prices. It explains the considerable time lag over which these costs of living factor into the government’s CPI. The extreme lag between actual costs and changes in CPI is one reason we know overall CPI will likely keep rising. Another thing to consider is that, when housing prices for homeowners rise 20% this month over the same time last year, that is never a 20% cost-of-living increase for everyone. It only affects those people who bought a home this month. So, if 0.1% of all the people in the US bought a new home this month, the formula used would have to average that rise across all of the people who saw no increase in their mortgage payments, except for their property-tax portion, as well as those whose homes are paid off. One of the big advantages of ownership is that your monthly cost gets locked in for years to come, so it doesn’t rise like rents. Also, your home is an asset, so when you sell it, all that housing inflation goes into your pocket as a growth in the value of your asset. That’s why the U.S. Bureau of Labor Statistics prefers to use a different metric by not looking at home prices at all. Instead, the homeowner side of CPI is only calculated by a survey asking homeowners to guess what their house would rent for (Owner Equivalent Rent), but who knows less about what any house rents for than someone who has owned their own home for several years to where they have not been paying attention to rental rates, especially when current rents have been skyrocketing? So, it’s a best guess by the least-informed people. And how tight is the correlation between what their house would rent for and what it costs? OER is more fiction than fact.

by Wolf Richter on Wolf Street:

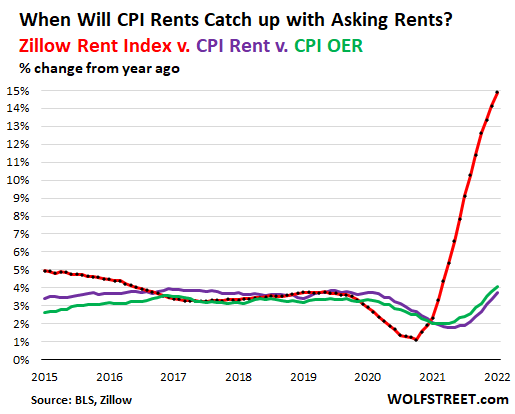

Two rent factors account for 32% of the Consumer Price Index. Despite the massive spike in “asking rents” across the US, those two CPI rent factors have been much lower than CPI and have thereby repressed CPI so far. Unlike asking rents, these two rent factors track the average rent that tenants are actually paying across the entire stock of rental units in US cities, including in rent-controlled units.

On the other hand, “asking rents” reflect current price tags on units listed for rent that people have not yet rented, and it takes a while for people to rent these units and pay those rents in large enough numbers to where they move the needle of the average rent actually paid across the entire stock of US rental units, which then gets picked up by the CPI rent measures.

But those two CPI rent factors are bound to catch up with asking rents and they will then fuel overall CPI – which was already 7.5% in January, WHOOSH.

But when will the spike in asking rents drive up CPI? And how much will it add to CPI?

The short answer: The current spikes in asking rents that have already occurred through January 2022 will add more than 1 percentage point to overall CPI for the year 2022, and will add more than 1 percentage point to overall CPI in 2023, even if asking rents don’t rise further from here. This is already baked into the numbers. CPI is going to catch up with a painful reality spread over the next two years.

The asking-rent spikes are brutal.

Rents for single-family houses and condos on the rental market exploded by 12% year-over-year in the US, varying widely from city to city, the worst increase in the data which starts in 2004, according to CoreLogic today. Miami was on top of the list, with a 35% spike in rents. In the years between the Financial Crisis and the pandemic, rents of single-family houses in the US had been increasing in the 2.5% to 3.5% range.

Rents in apartment buildings – does not include single-family houses and condos for rent – jumped by 12% for one-bedroom apartments and by 14% for two-bedroom apartments on average across the US, according to Zumper data. In 20 of the 100 largest cities, rents spiked by 20% or more, and in 11 of them, rents spiked by 25% or more. This is based on median asking rents, which are the rents landlords advertise for their listings. They’re similar to price tags in a store.

By a different measure, the Zillow Observed Rent Index, rents in January spiked by 14.9% year-over-year across the US, varying widely among cities.

All these measures show the same thing: On average, rents across the US spiked by over 12% year-over-year, varying widely from city to city, with some cities experiencing astronomical rent increases.

Asking rents take 24 months to spread across CPI rent inflation.

Asking rents are the current price tags. They don’t show up in rent inflation until enough people signed leases for units at those rents, and are actually paying those rents in large enough numbers to move the needle for the entire stock of rental units in US cities.

This makes asking rents a leading indicator for CPI rent inflation. Turns out, according to a study by the San Francisco Fed, these surging asking rents that have already occurred will push up CPI rent inflation for the next 24 months.

The two rent measures in the Consumer Price Index that together account for 32% of the overall CPI show this lag, though they too have started rising. The CPI Rent of Primary Residence (“CPI Rent”) in January was up 3.8% year-over-year, and the CPI Owner’s Equivalent of Rent (“CPI OER”) was up 4.1%.

These two CPI rent measures track what tenants are actually paying in rent across the entire stock of rental units in the cities. This includes tenants in rent-controlled apartments where rents don’t rise sharply, and it includes tenants on still active leases where rents cannot be raised, and it includes tenants whose landlords are slow to raise rents for a variety of reasons, including to keep good tenants.

So, the CPI measures will not spike in the same magnitude as asking rents. Between 2017 and 2019, the CPI measures tracked closely with the Zillow index. But in 2015 and 2016, there were large differences: In January 2015, the Zillow index showed rent increases of 5%, while the CPI measures showed rent increases of 2.6% and 3.5%.

When will these asking rents start fueling overall CPI?

So far, the rent factors in CPI have repressed overall CPI. Overall CPI in January jumped by 7.5%, despite the low readings of the two rent factors – rent of primary residence (3.8%) and owner’s equivalent rent (4.1%).

The San Francisco Fed has now come out with a staff report to estimate when these asking rents would filter into the CPI rent measures, and thereby into overall CPI. And this is going to happen over the next 24 months bit by bit.

The asking rents that have already occurred will likely push up the CPI rent factor by 3.4 percentage points in 2022 and then again in 2023, and given the 32% weight of the rent factors, will add 1.1 percentage points to whatever CPI will be by the end of 2022 and will add 1.1 percentage points to overall CPI in 2023, even if no further rent increases occur in the market.

So any leveling off or even declines in the CPIs for new and used vehicles will pale, because of their much smaller weight, in comparison to the coming surge of the CPI rent factors.

In terms of the measure the Fed uses as inflation target, “core PCE,” whose housing components are smaller than in CPI, the asking rent spikes that have already occurred will add 0.5 percentage points to core PCE in both 2022 and 2023, according to the San Francisco Fed, even if no further rent increases occur in the market.

Crypto Millionaire: “Pay Attention to May 20th”

Charlie Shrem is like the “Godfather of Cryptocurrencies”. He discovered Bitcoin when it was trading for $5. Ethereum at $109. Binance at just $6. Cardano for 5 CENTS. Today, he’s sharing the details of a $0.21 CENT crypto with Top 5 Potential… as well as his BIG prediction for May 20th.