It’s not easy being a mainstream economist. You spend your life building models that become your professional identity. And when those models fail to describe and predict reality, you’re left wondering about the meaning of it all.

The latest case in point is US housing. Keynesian economic models say that if you lower mortgage rates you get more houses bought, sold and built. A nice, simple piece of cause and effect. But today’s mortgage rates are at levels that would have incited a buying frenzy a generation ago, employment is rising — and home sales, home building and mortgage originations are all flat-lining.

Zero Hedge and Automatic Earth recently posted good discussions of the current state of the housing market. See:

Economists Stunned By Housing Fade

US Housing is Down For the Count

Both articles conclude that housing is weak and getting weaker. But the real question is what this means for the rest of the economy. Is housing a discrete sector dealing with its own supply/demand issues, or is it a sign of things to come for consumer spending, government tax revenues, and business investment?

The argument for the latter scenario is based on the idea that newly-created currency pouring into the financial system pumps up asset prices, which convinces people that they’re rich enough to indulge in new cars, new clothes and nice vacations — and more stocks, bonds and houses.

But this “wealth effect” only works when the amount of debt in the system is low enough for new paper profits to change behavior. If people already carry too much debt, then they don’t feel comfortable borrowing even at historically low interest rates, and inflated asset prices become harder and harder to support. Either they stall or start moving lower, which shifts the wealth effect into reverse and sucks the air out of the economy.

The reason that so many economists didn’t see housing rolling over and don’t think it will affect the rest of the system in any event is that most Keynesian models don’t pay attention to society’s balance sheet. A given amount of new debt is supposed to increase “aggregate demand” by the same amount whether the government and consumers are debt-free or buried under a mountain of obligations taken on in years past. That’s a false assumption of course. Liabilities matter, and the fact that debt levels, especially student loans, are hitting records probably explains why housing isn’t behaving according to script.

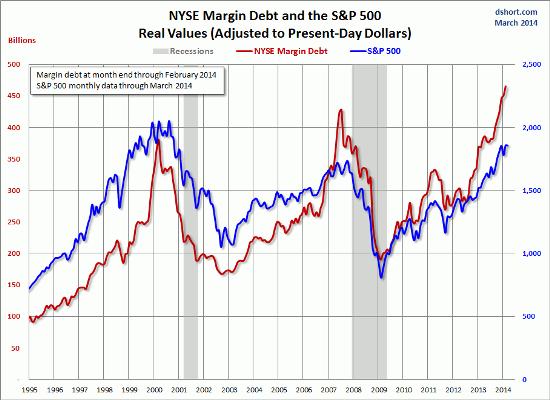

The other fuel for a wealth effect-driven boom is the stock market. Here again, a nice pop has coincided with a big jump in debt, in this case margin debt, which investors incur when they borrow against stocks to buy more stocks. Late last year margin debt hit a new record and since then has gone even higher. Now it’s at levels that, based on history, imply less bang for each new borrowed dollar. Going forward it will be harder for investors to generate big returns by borrowing money and buying more equities. Taking profits will begin to seem more and more prudent, until sellers swamp buyers and the markets correct.

Click here for a great explanation of why pretty much every stock market valuation measure is now flashing either yellow or red, from John Hussman.

Assuming that equities plateau or start falling, what does that do mean for government’s strategy of using asset bubbles to pump up the consumer economy? Probably it derails it. The question is when.

Hussman notes that periods of extreme overvaluation like today are good indicators of low average stock market returns over the next decade, but not necessarily great trading signals. Stocks might get more overvalued before they stop. But that would raise the risk of a crash, which would have an even more serious impact on investor psyches. So either way, this year or next, the wealth effect will become the poverty effect, and asset owners will become asset sellers.

26 thoughts on "Why Housing Has Stalled — And Why Everything Else Will Follow"

The subprime lending has officially returned in a last ditch attempt to prevent this bubble from popping. Illinois just announced the “Welcome home Illinois” program. First time buyer will be given $7500 to put down on a house and will only be required to put down $1000 of their own money. As long as you have not purchased in the last three years, you will be considered a first time homebuyer. Have we not learned the lessons of the past. They not be satisfied until they blow this financial system and housing market into pieces.

The subprime lending has officially returned in a last ditch attempt to prevent this bubble from popping. Illinois just announced the “Welcome home Illinois” program. First time buyer will be given $7500 to put down on a house and will only be required to put down $1000 of their own money. As long as you have not purchased in the last three years, you will be considered a first time homebuyer. Have we not learned the lessons of the past. They not be satisfied until they blow this financial system and housing market into pieces.

50% of non-owner occupied RE is being bought in all cash purchases w/ credit @ record lows…this is a clear signal that those who used to look to fixed income markets (bonds) have entirely moved their “safe” money to RE looking only for cash flow, not leveraging up. However, rents (derived from income/savings vs. leverage/credit for mortgages) are now nationally moving above 35% of pre-tax income. On a post tax basis and including utilities and other costs to renters, there rent / utilities are taking above 50% of their post tax median household income. These high rents (coupled w/ flat household incomes since ’07) also reduce renters ability to save to ultimately become buyers.

This rent vs. prices is crushing the 35.5% of renters are being forced to choose between paying their rent or spending in the economy…money / wealth is being transferred from the non-asset owners upward where it is not being leveraged or used to consume…

I find it interesting economics can accomplish little more than detail rationalizations as to why the other guy is wrong. After a couple of decades watching the adversarial rants, I don’t consider economics a “science” in any real sense of the word. A mess of contradictory opinions is more like it. So when things are going my way, I’m an “expert”. Works like that in my life too. But when it isn’t going my way, I hunt for something removed from me to be at fault. Unfortunately, I’m not enough of a “name” to have a blog so my opinions are meaningless. My point is opinions are opinions and rarely have anything to do with reality. All the reality twisting rationalizations in the world won’t change that.

John, you might want to add the Debt-to-Income Trap to your list. DTI is getting worse thanks to The Fed. Stagnant wages and rising home prices. Thanks Ben and Janet! http://confoundedinterest.wordpress.com/2014/04/29/ready-to-grumble-since-2009-hourly-wage-growth-plunges-42-while-reg-gas-rises-128-and-foodstuff-prices-rise-51/

i dont think the stock market is set to recover. i think there are social planners getting ready to replace the dollar with a new global currency and that it will happen some time next year.

“Employment is rising”? No, not really. Only the number is improving because people are going OFF the radar.

Housing price are too high.

Working like a charm! …. NOT!!! http://confoundedinterest.wordpress.com/2014/04/28/recovery-part-time-workers-replace-full-time-since-the-recession-bad-news-for-housing/

I’m not so sure that things are going to change much in the broad economy either way in the next year or two.

First of all, I don’t think the “wealth effect” operated much over the last few years and I don’t think a reverse wealth effect will manifest either even if housing and/or the stock market rolls over. Most people just don’t have that many options. Most haven’t had much disposable income lately, so they haven’t been able to buy much in the way of non-essentials (and that includes saving and investing) regardless of housing prices or the stock market. It just hasn’t mattered because there hasn’t been enough disposable income to spend to make difference.

Secondly, most people (i.e., “Main Street”) who have earned “disposable” income have chosen to either save it as cash, or buy PMs, or have used it to pay down their debts if they had any. After all, every dollar spent paying down a debt balance that charges, say, 5% interest is equivalent to earning 5% on that amount in a literally risk-free investment, and actually even higher than that when you do adjust for risk and account for taxes.

Therefore, even if housing and the stock markets roll over I don’t think it’s going to matter to most people because they will still do the same things they’re doing now. That doesn’t mean it won’t change things for RE and stock owners, but that’s clearly shown to not constitute the overall economy, only on the margin.

I think even the most inveterate stock investor and talking head would agree (and has pretty much all along since 2010) that unless the overall economy improves substantially (and very, very soon at this point) then asset values are going to fall again almost regardless of what the Fed/CBs do. Both assets increased because an improving economy was assumed and investments were made accordingly. It could all start to unwind for those folks (which would be a big deal for them) but it probably won’t affect most people because they don’t have much to lose, except maybe on paper.

Been covering the housing market “recovery” for a year at Smaulgld.com.

Google “The housing recovery that never was, is over” for a recap of this artificially created recovery in price only. Now higher prices are also in jeopardy.

Great article. Throw in the bursting of the debt bubble and the decline in real incomes (along with money velocity) and you can see the end. http://confoundedinterest.wordpress.com/2014/04/25/m1-multiplier-and-m2-velocity-drop-to-all-time-lows-the-burst-of-the-great-american-debt-bubble/

Not much to disagree with here. There are any number of potential triggers/proximate causes for the next downturn in equities and real estate, but one of the most powerful surely has to be what the Fed ultimately decides with respect to QE and interest rates.

The FOMC has painted itself into a corner. If it continues the taper, it’ll eventually be reflected in higher interest rates for Treasury and other debt instruments, which will end up reversing the gains in equities and reversing the recent run-up in real estate prices as mortgage rates continue to rise. If the Fed pauses or reverses course on the taper, it’ll have kicked the can a bit but done nothing to solve its QE exit problem – all while gold, the canary in the coal mine – squawks even louder.

With six more FOMC meetings left in 2014, it’s hard to see how we don’t end up with either an equities/RE rout or higher gold prices. However, Yellen has made it painfully clear that QE will not end unless the economy “continues to improve.” Time and again, she’s made the cessation of QE contingent on things getting better and better. When it’s clear that’s not happening (i.e., even to her), she won’t hesitate to continue with more Kool-Aid.

And if/when QE soldiers on through the end of the year, all the know-nothings on CNBC, Bloomberg and Marketwatch will act as if it couldn’t possibly have been anticipated.