For a while there it looked like the US and its main trading partners had finally achieved escape velocity. Growth was up, inflation was poking through the Fed’s 2% target, and most measures of consumer sentiment were bordering on euphoric.

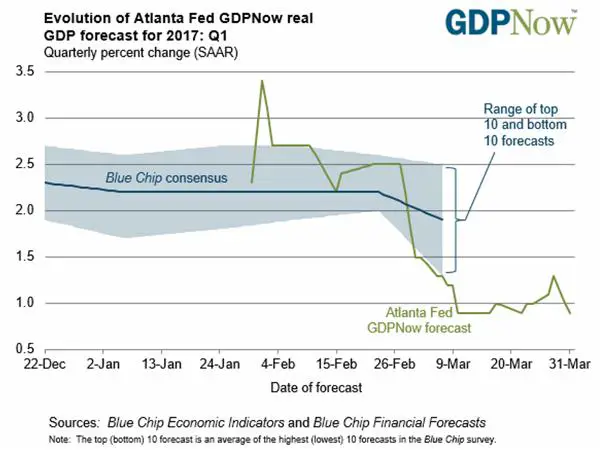

Then it all started to evaporate. Lackluster manufacturing and consumer spending reports sent the Atlanta Fed’s reading of Q1 GDP off a cliff to less than 1%:

And this morning the Wall Street Journal highlighted some recent changes in the yield curve that point towards further slowing:

Flatter Yield Curve in 2017 Shows Growth Concern Lingers

Long-term Treasury yields have declined modestly, while short-term yields have risen.A flattening of the Treasury yield curve in 2017 is a worrying sign for investors banking on resurgent U.S. inflation and growth.

Long-term Treasury yields, which are largely driven by the U.S. economic and inflation outlook, have declined modestly this year, following a sharp rise in the wake of the November election of Donald Trump as president. The 10-year U.S. Treasury yield has fallen to 2.396% from 2.446% at the end of 2016.

At the same time, short-term yields, which are more influenced by monetary policy, have risen in 2017 as Federal Reserve officials have made clear that they expect to continue raising the fed-funds rate through the rest of the year.

As a result, the yield premium on the 10-year note relative to the two-year note—known in the market as the 2-10 spread—slipped Wednesday to 1.107 percentage points, its lowest level since the election.FIRST QUARTER REPORT CARD

While the yield curve, like all market indicators, is subject to the ebb and flow of investor sentiment, economic data and political developments, a flattening yield curve gets special attention from investors world-wide because it can serve as an early signal of both economic slowing and overpricing in riskier asset classes.Those concerned that U.S. share prices were getting ahead of themselves took note in the first quarter when they “started to see the flattening of the yield curve,” said David Albrycht, president and CIO of Newfleet Asset Management, the fixed-income affiliate of Virtus Investment Partners . The Dow industrials have fallen 2% since hitting a record of 21115 on March 1.

Though economic data in the first quarter were mixed, many investors believe the flattening of the curve is the result of the unwinding of “Trump trade” bets that inflation and growth would pick up imminently with the adoption of tax cuts and fiscal stimulus President Donald Trump has promised. Hopes of a so-called reflationary agenda have been set back by the defeat in Congress of a White House sponsored health-care bill. That raised questions about whether Mr. Trump can get other legislation through Congress.

Expectations for higher long-term yields and a steeper curve rested on two pillars: first, that the economy on its own was showing signs of improvement, and second, that it would get an extra lift from promised tax cuts, infrastructure spending and regulatory relief.

At the outset of the second quarter, both of those pillars are still standing, yet neither is looking as sturdy as before.

The Journal goes on to note that the spreads between Treasuries and junk bonds are widening, which indicates growing fears of a slowdown-induced credit crunch. And that junk bond issuance is soaring, which implies a desire on the part of sub-investment-grade borrowers to raise cash while they can.

What’s happening? There are several possibilities:

1) There never really was a recovery. The post-election pop was, as the Journal asserts, just the human nervous system responding to a “new and improved” US government the way grocery store shoppers instinctively reach for boxes that promise a better version of an old stand-by. Now that the novelty has worn off, the markets are experiencing a “same corn flakes, different box” let-down. In which case 1% – 2% growth might be the ceiling, and debt/GDP will continue to soar world-wide. Make no mistake, this is an epic worst-case scenario.

2) Oil spiked in 2016, which led many to conclude that the global economy was growing because it was demanding more energy. But then crude gave back most of its gains, extinguishing the previous optimism and causing economic indicators like consumer spending to stall (because we’re all paying a bit less for gas lately). So risk-off: sell stocks and junk bonds, buy Treasuries. It’s no more complicated than that.

3) No one has the slightest idea what’s happening as insane levels of debt distort the models economists use to predict the future. From here on out, it’s unpleasant surprises all the way down.

Time will tell, but door number 3 is an increasingly safe bet.

24 thoughts on "Maybe The Recovery Wasn’t Real After All"

More money is made when markets CRASH

As a web developer I’ve taken Gordon T Long’s advice. I improve my skills every day. Our house of cards is going to crumble. However after the meltdown the world will continue to rely on the Internet as much or more than it does today. Work will pay off. For most people saved money won’t.

I think it’ll all work out as long as we print up 500 trillion in QE and then get those $10,000 hot dogs.

Not happening. I refuse to pay more then $9000 for a hot dog!

the only thing “achieved” was a delay of the inevitable and making it worse when the stuff finally does hit the fan.

the ‘recovery’ is an illusion/ smoke & mirrors created in the context of & brought about by ‘transitional sentiment’ (a debt-laden, infrastructure-based ‘recovery’, Promise of Tax Relief, Military Expenditure), superimposed upon a debt-based, ‘QE’ – ‘stabilization’ of the economy (& now the promise of Tax-Payer-funded, FED-Inspired, underpinning (Read Share-Purchase Programs from the Plunge-Protection Team) of the markets). Can U put brackets inside Brackets? – Is that degree of Concentration, etymologically legitimate? – Anyway the post GFC Debt-Ridden Structure was ”NEVER” unwound & everything within the Economy at large & since, has been about the use of Stimulus to kick the proverbial can down the road & forestall the dreadful day of reckoning – & That is without any consideration of Developments in our understanding of The Flat Energy Environment & issues relating to Energy Return On Energy Invested (”EROEI”/ EROI, cf Arnoux, St Angelo, etc) & it’s deeply troubling/ pessimistic implications for the Global Economy & it’s functioning.

So now, Corporates having bought back their own shares @ ‘peak-share-value’ & having totally destroyed The $$$Price-Discovery Mechanism (in ascertaining relative value), are busy issuing ‘Junk-Bonds’ to fund Divident payouts (Say ”PONZI-SCEME”) & The FED is about to tighten into all of this ‘Fragility’, relative weakness & chaotic madness,……….; QMAMBO13